Tax Planning Isn't a December Problem

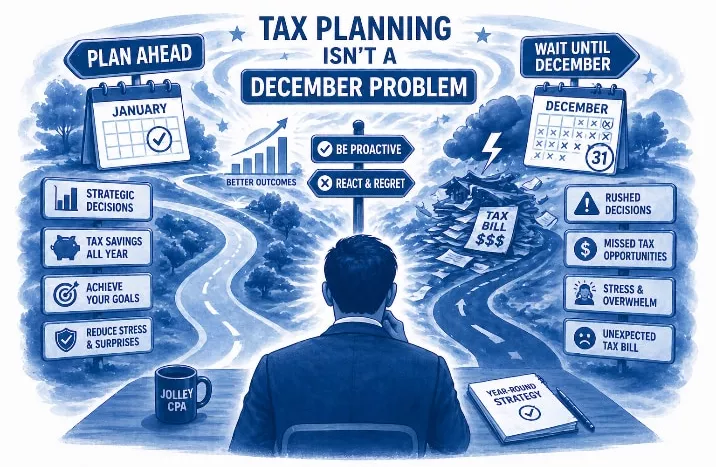

Most business owners think about taxes once a year, but real tax planning does not happen after the fact. This post explains why the biggest opportunities come from year-round visibility, monthly accounting integration, and acting before timing windows close.

INSIGHT FROM HAL JOLLEY, CPA & CFA

Tax Planning Isn't a December Problem

SUMMARY

Most business owners think about taxes once a year, somewhere between January and April. By the time they sit down with a CPA, the year is already over and most of the meaningful opportunities are already gone. That's the central problem with how tax planning is usually done — it happens after the fact, when there's nothing left to plan.

In this piece, Hal Jolley breaks down what real tax planning actually looks like: a year-round process integrated with a business's monthly accounting, divided between long-term structural strategy and year-by-year timing opportunities. The difference between the two approaches is the difference between filing a return and actually keeping more of your money.

“A common misconception is that tax planning happens at the end of the year. Looking back, it's often too late.”

— Hal Jolley, CPA & CFA

What I Actually Do for Clients

As a CPA, tax planning and tax preparation are obviously a big part of our practice. I prepare returns for clients' businesses and for them individually — it's the work they expect every year.

But when we integrate that service with monthly accounting for a business owner, something different happens. We're on top of the tax situation throughout the year. Not in March, not at year-end — throughout the year. That's the difference that ends up mattering most.

The Most Common Misconception

A common misconception people have is: I need to do tax planning right at the end of the year, or maybe in the first quarter of the next year.

“Looking back, oftentimes it's too late.”

That's the part that's hard for owners to hear, but it's true. By the time the year is over, most of what could have been done has already happened or hasn't. You can't go back and accelerate an expense in October if it's now February. The window has closed.

Tax filing can be done throughout the year, particularly when it's integrated with your investments — things like basis adjustments in your portfolio, for example. The mistake people make is thinking tax planning has to be one day at the end of the year. It can be — and should be — spread across the whole year. That's a common thing we do for clients.

Knowing Where You Stand: The Marginal Bracket Question

The second piece is this: when you know where you are financially through the year, you have a very good idea of whether you're around a marginal tax bracket or where you'll land at year-end.

That visibility unlocks something concrete. Timing adjustments — the ones that move you across or away from a bracket boundary — are usually use-it-or-lose-it. If you don't act before December 31, the opportunity disappears.

“These timing adjustments — they're usually use-it-or-lose-it.”

The Two Types of Tax Planning

When you're doing tax planning, you have basically two types of things.

Structural things you're doing to lower your taxes in the long term. And timing opportunities that are year-to-year.

Both matter, but they're different kinds of work. Structural strategy is the long-game stuff — entity choices, retirement vehicles, the foundational decisions that affect your tax position for years. Timing is the granular, in-year work — accelerating an expense, deferring income, harvesting a loss before year-end.

If you do tax planning as part of a process, some years you can avail yourself of a slightly lower bracket just by accelerating some expenses. Had you not done that, that opportunity probably goes away — because you may be in a different bracket in the following year.

“Some years you can avail yourself of a slightly lower bracket just by accelerating some expenses. Had you not done that, that opportunity probably goes away.”

Why a Process Beats a Once-a-Year Meeting

This is the case for treating tax planning as ongoing instead of seasonal. Each year, the structural pieces stay roughly the same — but the timing opportunities are different every year, and they only show up if someone is paying attention.

That's what integration with monthly accounting actually delivers. Not a tax planning meeting in November. A continuous awareness of where you are, where you're heading, and what doors are still open before they close.

Want to Talk?

If you've only ever done tax planning at year-end — or worse, after year-end — there's a good chance you've been leaving real money on the table for years without knowing it. A short conversation is the easiest way to find out what a continuous tax planning process would look like for your business.

More Topics

Financial Insights Business ServicesFinancial ForecastingFinancial PlanningTax PreparationWealth ManagementStart with a Complimentary Conversation

A no-cost discussion to understand your goals, evaluate your current strategy, and outline next steps.

Schedule a Complimentary Call